Burnham Holdings is the parent company of a family of boiler manufacturers. Among them you might recognize U.S. Boiler and Burnham. They also own Thermo Pride (furnaces), Thermal InMotion (rental boiler biz) and CSI Services (HVAC service). They enjoy strong brand recognition, allowing them to leverage their vast distribution network to introduce new products and gain faster product acceptance in the market. Currently, the family of boiler manufacturers have 33% market share for residential boilers (Annual Shareholders Meeting), highlighting its strong brand recognition and popularity among contractors. 75% of revenues come from Residential, while the remaining 25% comes from Commercial.

Burnham offers a compelling risk-reward opportunity, trading at 5x EBIT and at 62% of book value in a stable, growing industry driven by replacement demand which offsets any weakness in new construction demand.

Snapshot

Price: $13.6

Market Cap: $63m

EV: $84m

Shares Outstanding: 4.6m

Burnham operates in a stable, growing industry that is mainly driven by replacement demand. Revenues by segment are as follows: 70-75% is residential, while 25-30% is from commercial. 80-85% of revenues can be attributable to replacement demand while the remaining 15-20% is attributable to new construction. This is very attractive as any weakness caused by new construction is easily offset by replacement revenues. The average life of a boiler can be 15-20 years, in some cases even more. However, with high efficiency boilers taking the spotlight, these usually have a shorter life span which should accelerate the replacement cycle. The life of HVAC units has gone from 20 years in 2011 to 16.4 years in 2023.

We should see that with higher efficiency units, the average life should come down and increase the rate of the replacement cycle, resulting in consistent industry growth.

Currently we are seeing strong growth on the commercial side due to replacements of older, less efficient boilers. Commercial customers are more incentivized to save on operating costs than residential. The residential segment is experiencing weakness with the first two quarters posting YoY declines while the third quarter showed recovery, posting an increase in sales YoY.

The graph above shows the % of installed base replaced each year and the age of the HVAC equipment being replaced. It shows there is still a bunch of old equipment waiting to be replaced. Age of equipment is above trend while % of install based replaced below trend, highlighting the temporary weakness in 2022-2023. Additionally, the analysis done by bdools2 in VIC on his write up for Watsco he mentions “Assuming most systems replaced in any given year are 10-15 years old (some outliers outside of this) makes today’s core replacement cohort being units installed in 2008-2013, when shipment volumes were suppressed by the GFC housing crash. During those six years, 33.5 million AC and heat pump units were shipped. Since that time, annual shipments have steadily risen. Eventually we will be replacing the 2017-2022 cohort of shipments which amounts to 54.4m units. This is a volume increase of 62% between equal cohorts.” There are a lot of units that will be replaced in the coming years that were installed years ago. The construction boom post-GFC should start replacing in the next 3-6 years. He also mentions how the CEO of Watsco highlights the fact that replacement of HVAC systems is making more economic sense than repairing the systems. “Management has stated that the cost to repair has inflated more than the cost to replace, making it less economic to repair given the superior efficiency of new systems against old AC systems at a time when monthly budgets are tight and energy bills can be high. Contractors prefer and favor replacements in their advice to consumers, which makes it unlikely to see an extreme shift towards repairs.”

With Burnham having 33% of the boiler market in the US, they are well positioned to benefit from adoption of high efficiency boilers and electrification. Recently, they launched Ambient, which is their family of electric heating products. This includes an electric boiler, meeting demand for the decarbonization of buildings, and also a heat pump which has experienced significant growth over the years.

In 2023, the boiler market experienced a decline in units shipped as experienced by A.O. Smith, which owns Lochinvar, a competitor of Burnham's boiler family. In contrast, in 2023 Burnham was able to grow when the industry declined, showing market share gains.

Production Capacity Expansion

In early 2024, Burnham expanded production capacity by building a 45,000 sq ft facility adjacent to their U.S. Boiler manufacturing facility in Lancaster. This was not disclosed by the company in quarterly or annual reports, so I am not sure many investors are aware of this, but they did it to expand production of their Alta boilers which is a best seller and accounts for roughly 75% of their high efficiency boiler sales in 2023.

We can imply that they will keep seeing strong demand and taking market share. This goes hand in hand with A.O. Smith facility expansion for their water heaters and boilers, as they expect further demand to materialize.

Borrowing Capacity Expansion

In the 2023 annual letter to shareholders, Chris Drew announced the expansion of borrowing capacity by 33% which is the first increase in their borrowing capacity since 2005. This should signal better times ahead, and demand that will end up materializing as the replacement cycle fastens. “Working with our banking partners we entered into a suite of new credit agreements that expand our borrowing capacity by 33%. This is the first increase in our credit facilities since 2005 and the increased capacity is available to support our continued growth and segment expansion.”

New CEO

Chris Drew had his first full year as CEO in 2023, where he was able to achieve record revenues and profits for Burnham. Chris has extensive knowledge of the industry and served as the chairman of the AHRI, which is the industry trade group.

New Construction

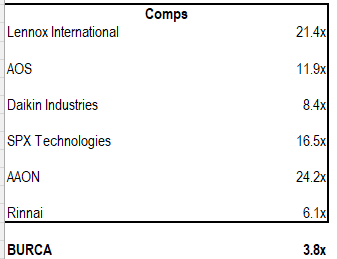

It is no secret that the housing market is in a pile of dirt right now, and with the future around tariffs uncertain, we just don’t know what will happen with housing. Considering that, it is very likely that Burnham is underearning as 15-20% of revenues come from new construction. They are showing great performance currently, but with a strong housing market the full earnings power should come out. Either way, in current conditions, you are buying the business for 3.8x EBITDA which is a bargain compared to comps.

Warranted, Burnham should probably trade at a discount, but the average of the peers come to 14.75x EBITDA, making BURCA’s current multiple illogical. It is a prime acquisition target, and I wonder if management is willing to sell at the right price.

The industry should continue to grow as people will continue to need to heat their homes up. The constant replacement cycle and current and future upgrading cycle to high efficiency systems makes it an attractive investment. Additionally, there are significant tailwinds if and when the housing market recovers where we will be seeing more housing starts and more existing home sales which should boost replacement of HVAC systems. Burnham is well positioned to continue grabbing market share as they shifted their focus to new product development throughout the years, ensuring they keep up with competition and also exceed them.

Valuation

At 4.4x 2024 EBIT and a current dividend yield of 6.8%, I consider BURCA a big bargain given its strong market share in residential, their vast distribution network, and contractor relations. In the coming years as the industry grows and the replacement cycle accelerates, Burnham is well positioned to grab market share. We are seeing early signs of preparations which include the facility expansion and also the borrowing capacity expansion.

I believe that a 10x EBIT multiple is fair for a company like Burnham. As mentioned before, they have a big market share in their respective market which warrants a higher multiple. Not to mention, the last few years performance has been very good and last FY broke record revenues and profits. With a 10x multiple we come up with a price of $31.43, which implies an upside of 131% or a 5-year CAGR of 19%.

Risks

Warmer weather

Competition

Slower replacement cycle

New Construction pivoting to Heat Pumps

Sources:

How Long Will My Boiler Last? | Temprite Climate Solutions

*Disclaimer: The information provided in this write-up is for informational and educational purposes only. It should not be considered as financial advice or a recommendation to buy, sell, or hold any security. The author is not a licensed financial advisor and does not purport to provide professional investment advice. The analysis presented is based on the author's personal research and opinions, which may be subject to errors, omissions, or changes without notice. Any investment decisions should be made after conducting your own thorough research and consulting with a qualified financial professional. The author and any associated parties are not responsible for any financial or other losses incurred based on the information provided in this document. Past performance is not indicative of future results. Always consider your personal financial situation, risk tolerance, and investment objectives before making any investment decisions.

You had good timing doing a write up on this stock. Gabelli started buying shares. The stock is not very liquid. The company has two classes of stock as well. They also still have a defined benefit plan, but I believe it is frozen.

The new boilers may be more efficient, but the new more energy efficient boilers do not last as long and typically will need to be replaced a lot sooner, whereas the old conventional boilers could last over 35-40 years. The record for a Burnham boiler was 70 years in New England no less.

I believe the dividend is high because much of it goes to family members. They have a state of the art manufacturing plant in the Carolina’s.

A long time ago there were rumors it might be sold to Buderus. Most of the pricing is done via dealers through heating oil companies. I believe but don’t take my word on it, the threat would be to more natural gas conversions.

You seem more current on the company, so I hope you post updates.

Nice write up. Company is still undervalued even with the move in price, IMO. They usually express this themselves in filings and letters as well.

One more thing, being connected to the housing market, I have seen the shares trade quite lower, during recessions or problems in the housing market. That should be a logical deduction. However, they have held the dividend historically through thick and thin.