Conrad Industries

An Aging Fleet and The Coming Replacement Cycle

At a $60M market cap and $26M EV, Conrad Industries trades at just 2.9x FY24E EBIT (~$9M), as it enters the early stages of a major barge replacement cycle. With industry tailwinds driving an all-time high backlog and a rock-solid balance sheet (cash >50% of market cap), I believe Conrad is poised to surpass prior peak EBIT ($30M+), offering a highly compelling risk/reward opportunity.

Overview

Conrad industries operate five shipyards in Louisiana and Texas and operates two segments: New Construction and Repair & Maintenance.

The New Construction segment focuses on building a variety of vessels including barges, tugboats, ferries, etc. Repair & Maintenance segment focuses on repairing existing vessels, maintaining them, and sometimes converting the vessels into a different purpose vessel.

The US shipbuilding industry is protected by the Jones Act. The Jones Act requires that vessels that transport goods or passengers between two US ports, be built in the US, owned and crewed by US citizens. Given that, most of their business comes from Inland operators that transport goods through the US Inland Waterways and the government.

Credits to Phenom Capital who has a great write-up on the company and re-sparked my interest to dive in. He gives great insights on the situation and would encourage everyone to check it out. I will just be following through on some points.

Replacement Cycle

I believe there is a super replacement cycle starting for inland dry and tank/liquid barges with the fleet aging to levels that cannot be ignored for much longer. With capacity for shipyards currently almost full, operators wanting to replace their old fleet will have a hard time getting deliveries soon as they compete for capacity. Arcosa, which is the largest barge maker, mentioned on their Q4 2024 EC “On hopper barges, we have backlogs through the third quarter. On tank barges, we're sold out for 2025, and with some additional orders booked since the end of the quarter, at the current production rate, our delivery time for a new tank barge order goes deep into 2026.” This situation is not favorable for barge operators as if they keep deferring the replacement of their fleet, they run the risk of 1) Rising steel prices which will make replacement even more costly, and 2) Operating with a smaller fleet due to retirement of the fleet and not being able to receive delivery on a timely manner.

The age of the barge fleet keeps getting older, and if operators keep delaying it, it will just pronounce the cycle even more.

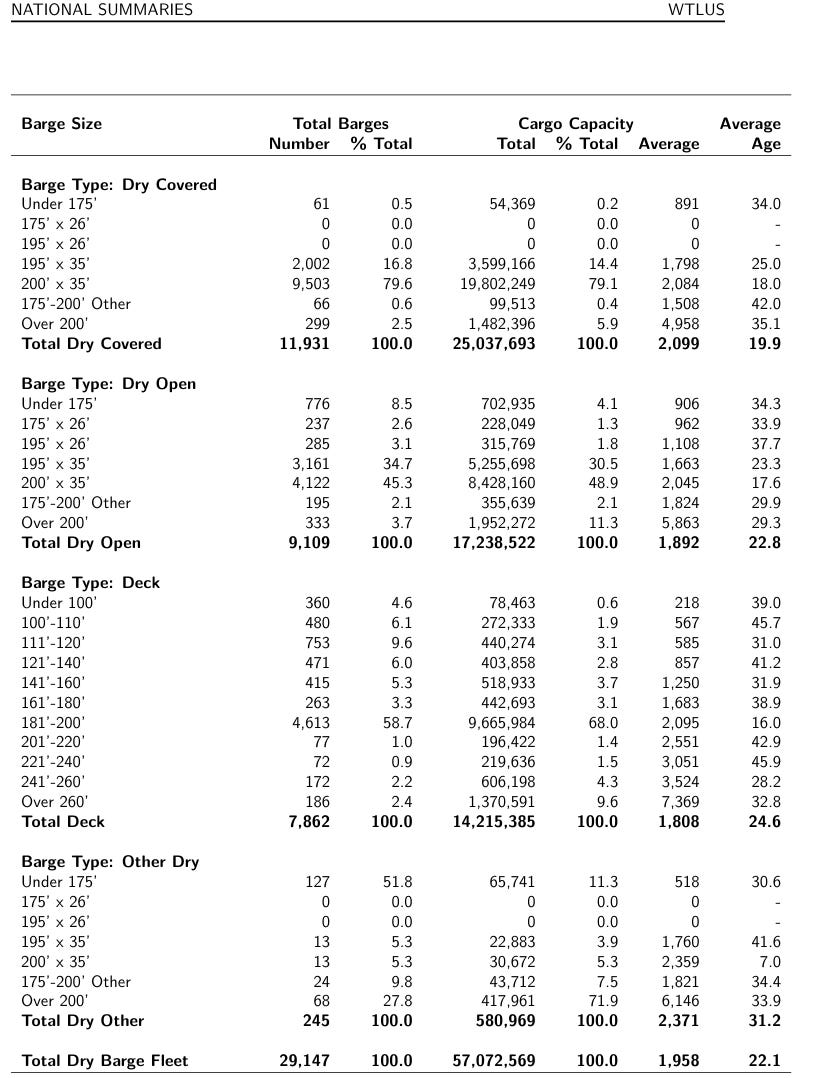

These graphs come from data from the US Army Corps of Engineers and we can see the difference from 2013 data to 2022 data (Top two graphs).

For tank/liquid barges we can see we have significantly more barges in the 16-25> due to the big construction cycle for tank/liquid barges during the 2010-2014 shale boom period. As time went by, new construction significantly decreased causing the fleet to age and now have nearly 30% of the fleet older than 25 years old and nearly 10% being 21-25 years old. The average age of the tank fleet is now at 20.5 years.

On the dry side we have more than 30% of barges older than 25 years old, 20% from 21-25, and 10% from 16-20. The dry side new construction has been a more depressed market due to significant underinvestment in the fleet as evidenced by the graph above. The average age of the dry fleet is 22.1 years.

USACE Digital Library - USACE Digital Library

The picture above shows the total new construction in a given year. If you look at 2013, the number of barges being built were 400% higher than what were built in 2022. With the rise in steel prices in 2021-2023, it delayed significant replacement needs which has carried over to today, leading me to believe the cycle has just started.

The positive is that the thesis does not even factor in expansion of the fleet. Frankly, I'm not sure if there will be expansion of the fleet but with the current administration planning to propose an Office of Shipbuilding and Trump trying to revive the US Shipbuilding industry, you never know. But that is too speculative to even factor in.

Kirby, which is the largest barge operator, has said that in order for them to expand the fleet, barge rates have to go up an additional 40%. Barge rates have been going up according to them and they forecast 2025 would be another good year for them as supply is as in check as they have ever seen. From their Q4 2024 EC “The 2025 order book, we think is lined up to be about 50 to 60 inland barges. But I will tell you that at 50 to 60 new construction orders, the present shipyard capacity that can build a high quality inland tank barge is full. If you wanted to build another barge beyond that 50 or 60, you're well into 2026 to get delivery. So I think the capacity to build inland barges in the United States is diminished from what it was once upon a time when we saw the hyper-aggressive building during the days of chasing the shale crude barrel. So supply is as in check as I've ever seen it in my 28 years.”

“So I think when you compound all that or add all that together, you've got a supply side that looks as good as we've ever seen it, as I've ever seen it. And you're clipping along at 75 barges retired in 2024. And if you take that 40, 41, 42-year old barge group as a group, I mean, you still got 500 plus barges that need to retire in the next five years. So I think when you bake all that together, supply size is in check as we've ever seen it.”

From Q3 2024 EC “And then with retirements, you’re seeing us going to retire some barges. I think the industry is going to retire a fair number of barges. So we may actually see from a supply standpoint, a net contraction in the number of barges out there.”

According to Kirby, around 47% of the inland tank barge fleet has to go through its COI (Certificate of Inspection) renewal, so there is probably going to be a good amount of barges being retired, further tightening the supply of tank barges as they come to the conclusion that these barges are not feasible to continue operations further setting up the super cycle and possibly lead to an accelerated replacement cycle.

The decrease in supply of barges obviously benefits Kirby as it increases the barge rates and since they are the largest operators, they have way more barges than smaller subscale operators. They benefit from that dynamic as well.

Another positive for the industry is that barge utilization rates are in the 90%+ range which should incentivize new construction in theory. On the dry side, Kirby mentions increased new construction for hopper barges in Q3 2024 “And so, I think there’s also a large number of hopper barges being built to replace on the dry cargo side of the business. Those hopper barges compete for the capacity for new construction with tank barges.”

The commentary on these earning calls of these industry players is very valuable and forward-looking. There is so much more I want to quote from Kirby’s and Arcosa’s ECs. I encourage everyone that’s interested to go listen to them as it perfectly explains the dynamics in play right now.

Cost of Construction

The biggest headwind right now is the price of steel as it is still elevated for barge operators to justify new construction. Labor costs are also higher with Conrad raising hourly labor rate to their workers in February 2024 to retain their workforce. That's a whole other issue that will come by itself if the shipbuilding industry expands, the lack of workers.

Luckily with the incoming replacement demand coming from commercial customers mainly, they will have some protection if steel prices do move up, as they have provisions that protect them from that but not from escalations in other costs.

The big losses in 2022 and 2023 stem from the surge in steel prices during that period, affecting their fixed price contract with the Navy to build eight YRBM barges. Since then, steel prices have subsided and for the nine months ending FY24, they have been profitable generating ~7m in operating income. There is definitely uncertainty with steel prices and all the tariffs announcements that can be inflationary. The future on the cost side remains uncertain. But with better priced contracts moving forward and shipyard capacity likely full, they can focus on adding profitable backlog as they now have the pricing power.

Valuation

The company is currently trading at $60m market cap, with $3.25m in debt, and $37.45m in cash bringing the EV to $26m. Now, they generated $7m EBIT during the nine months, bringing run rate EBIT for the full year to $9m. This brings FY24 EV/EBIT 2.9x at the start of a super cycle.

In this cycle, the company should be able to at least replicate the prior 2010-2014 cycle. Prior peak they generated $30-$40m in EBIT, which should result in mid cycle EBIT to $15-$20m. However, I believe this is just the early stages of a super cycle and currently are generating $9m run rate EBIT. If we assume they generate prior peak EBIT at $30m, this brings mid cycle EBIT to $15m, only paying 1.7x EBIT. Peak EBIT would be less than 1x EBIT. Given the current dynamics, they should be able to surpass prior peaks as there is significant pent-up demand to replace the fleet, but steel and labor costs remain as headwinds in order activity. Despite this, they achieved the highest backlog in the company's history at $310m.

At 6x mid cycle EBIT, we get a share price of $24.75. At a 10x multiple, we get a share price of $36.71. I believe 10x is appropriate as I believe this cycle will be long and way stronger than past cycles. I also believe I was very conservative in the mid-cycle EBIT numbers. If we assume they can operate without any significant forward losses moving forward and we back out the losses on the YRBM barges for the nine months FY24 then we get to a run rate EBIT number of $23m. Keep in mind this is during the start of a big replacement cycle coming, not the mid or peak. You start playing around with the model and backing out losses and you can see significantly more upside. I won’t factor that in the model to be conservative, but I don’t think that's out of the picture and gives a sense to what we can see moving forward.

Conclusion

Conrad is trading at dirt cheap levels with a significant replacement cycle in front of them. The barge fleet is aging and there will be a lot of retirements of the fleet in the coming years, making the supply of barges even tighter than what it is today. Utilization rate for the operators is at 90% range which should incentivize them to replace the fleet and even expand as barge rates go higher. Any delays on the replacement cycle will just put a strain on the operators as delivery dates extend into 2026-2027, making them compete for capacity with other operators. Steel prices and labor cost remains a headwind, but operators probably cannot defer replacement for much longer.

RISKS

Tariffs affecting the transportation of commodities

Delays in the replacement cycle

Steel prices

Do you foresee that tariffs will also cause steel prices to go up which will affect the fixed price contracts ?

is the backlog mostly price fixed, or do they have any inflation protection clauses?

" future on the cost side remains uncertain. But with better priced contracts moving forward and shipyard capacity likely full, they can focus on adding profitable backlog as they now have the pricing power."

"The big losses in 2022 and 2023 stem from the surge in steel prices during that period, affecting their fixed price contract with the Navy to build eight YRBM barge"